Stop losing money to the nursing home.

Don't worry if your loved one is already in a nursing home; it's never too late to protect your assets. Get started by answering a few questions about your situation.

At Senior Care Counsel, we help seniors and their families find financial relief from long-term care expenses, even if they're already in the nursing home. We offer the resources needed to navigate your situation with care and confidence, including matching you with a dedicated long-term care planning professional in your area.

You and your family have options. Connect with us to learn more.

How It Works

We match families with long-term care planning professionals who specialize in protecting your assets from the nursing home.

Answer

Start by answering some quick questions about your situation.

Connect

We'll match you with the professional best suited for your unique circumstances.

Plan

You'll work with your professional to develop the asset protection plan that's right for you.

Resources

Not ready to connect? Browse our resources to get a better understanding of long-term care planning.

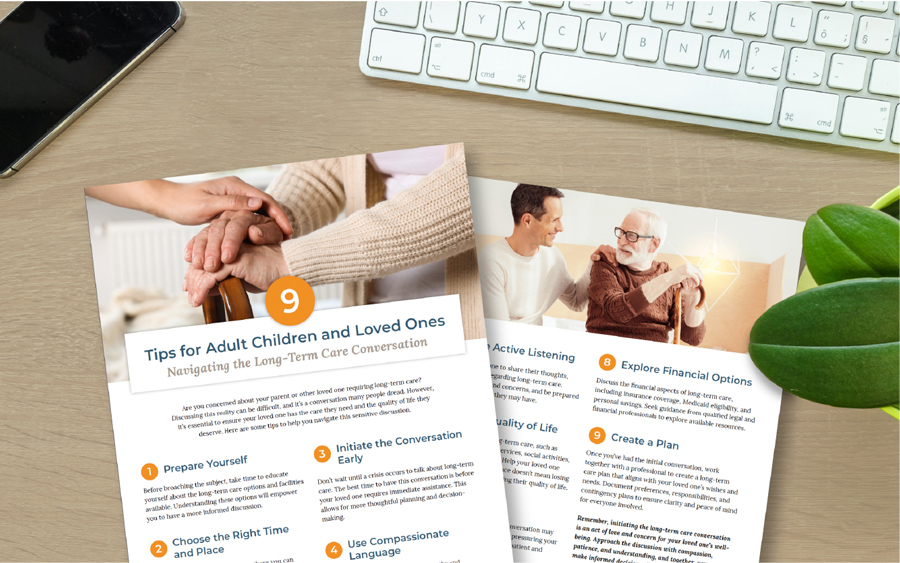

Having The Long-Term Care Conversation

Check out tips for starting this crucial discussion with your loved one.

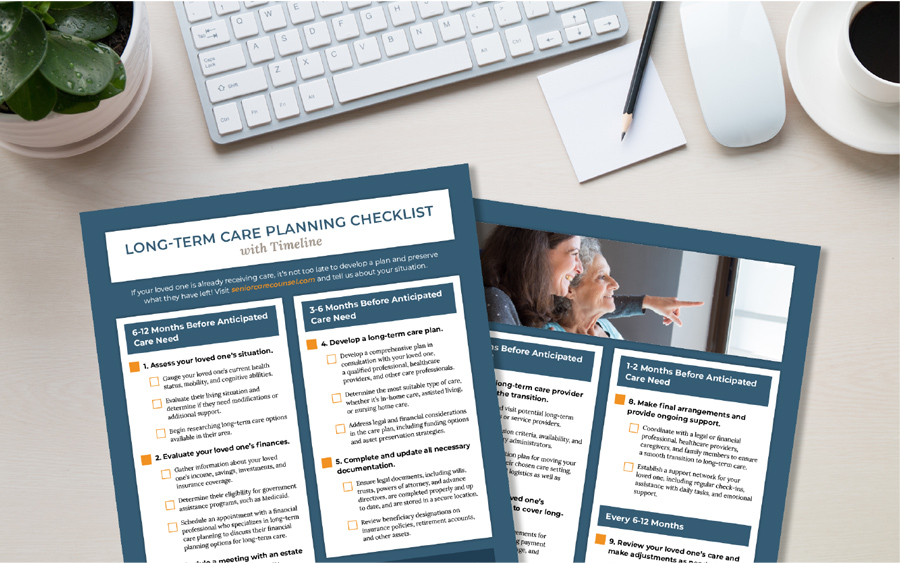

Long-Term Care Planning Checklist

Here's a timeline to follow if your loved one will need care in the next year.

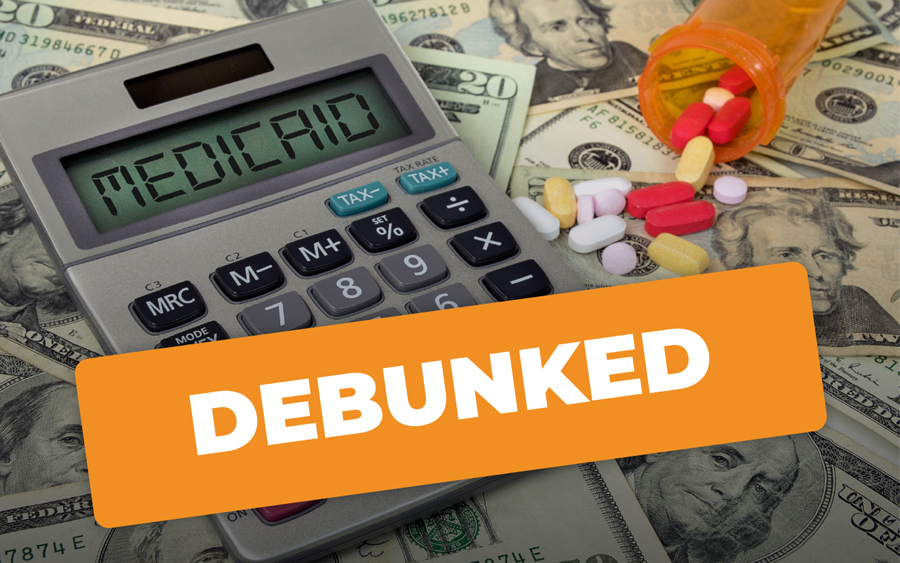

Common Medicaid Myths: Debunked

Allow us to dispel some common myths surrounding the Medicaid program.

Take the Savings Quiz

Discover how much you or your loved one could save with a proper long-term care plan.

Why Work with a Professional?

Learn why you should work with a qualified professional in the planning process.

Who We Are

Our mission is to educate families on the options available to them. Despite what the nursing home says, it's never too late to protect your assets.

Trending Topics

Explore topics related to long-term care planning, the Medicaid program, and more.